Choosing Your Financial Caregiving Role

Explore eight financial caregiving roles with different levels of access and responsibility to find the best fit for supporting your loved one's finances.

Table of Contents

Introduction

As our parents age, we find ourselves stepping into new roles in their financial lives. Making this transition can be challenging. By understanding the available options for getting involved, you and your family can choose the right approach at the right time.

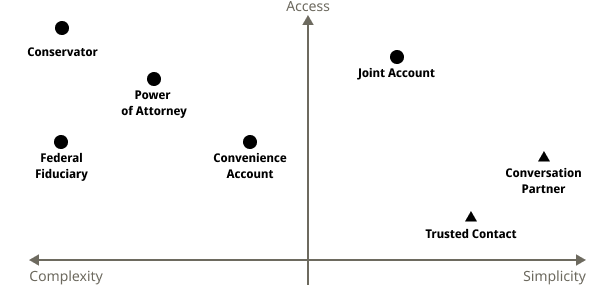

There are many roles (pictured below) to consider, each offering a different tradeoff between your access to the accounts and the requirements for establishing that access.

A spectrum of role options, where roles marked with circles have the ability to move money. Federal Fiduciary represents both the SSA Representative Payee and VA Fiduciary roles.

Roles that require legal documents, fiduciary duties, court appointments, or changes to the account ownership are considered more complex than those that do not; roles with more financial power and visibility are considered to have more access than those that with less visibility.

Let’s explore each of these roles in detail to help you determine which might be most appropriate for your situation and how to navigate the responsibilities that come with them.

Conversation Partner

The lowest level of involvement is simply being a conversation partner. This role is about getting everyone comfortable discussing finances and requires no changes to account access. Having regular conversations about finances can also help detect financial issues and mental decline earlier and better prepare your family for future emergencies.

Start by talking with your parents about why you’d like to be a part of their financial lives and what you would like that relationship to look like. Listen to what’s important to them and remind them of your support. As time goes on, you can gradually ask for more visibility into their account balances and transactions. The focus of this stage is to respect their independence while opening the door for more support in the future.

- Ask your parents to summarize which institutions they have accounts with

- Ask when the last time their advanced directives were updated

- Invite yourself on their next visit to their bank or financial advisor

- Offer to review their financial statements and bills together

- Discuss general financial goals and concerns

The first conversation will probably be uncomfortable, but building a routine around discussing finances now builds trust going forward and lays a solid foundation for the future.

Becoming your parent’s financial conversation partner is a great place to start providing financial care because they have full control of what information you see. At some point, however, you’ll want to have a direct relationship with their institutions to receive notifications about potential fraud and exploitation.

Trusted Contact

A step up from conversation partner is becoming a trusted contact on your parents’ financial accounts. This role allows financial institutions to contact you if they suspect fraud, notice unusual activity, spot potential financial exploitation, or cannot contact the account owner. These notifications act as an early warning system that respects your parents’ privacy.

A trusted contact has no direct visibility into the account, no ability to make transactions, and no claim of ownership of the account.

- FINRA, NASAA, and the SEC’s Office of Investor Education and Advocacy all advocate for setting up trusted contacts. Sharing content from these agencies, like this, is a great way to start the conversation.

- You may want to set a trusted contact for your own accounts. Try discussing your motivations for adding a contact with your parents.

- Some institutions will allow multiple people to be added as a trusted contact. If you’re already discussing expanding the care team to include other family members, include the trusted contact role in the conversation.

Not all financial institutions support adding a trusted contact, so you’ll need to contact each institution to see if and how your parents can add you.

You can focus search engines on a specific domain using the “site:” keyword. For example to search myinstitution.com for information about trusted contacts, enter

site:myinstitution.com trusted contact

Becoming your parents’ trusted contact is a good way to make your financial caregiving role more official without needing direct access to their accounts. This role, paired with good visibility into balances and transactions and healthy conversations, will be all you need until your parents require help managing their day-to-day finances.

Partial Access

You may eventually need to provide more hands-on help with specific accounts or benefits. When that time comes, there are several ways access an account while leaving ownership solely with your parents. Always consult with the relevant institutions or agencies for the most up-to-date information and requirements.

Convenience Accounts

Some financial institutions may offer convenience accounts, also known as agency accounts. Your parents are setup as the owners of the convenience account, while you are added as an additional signer. This allows you to use the account for your parents’ benefit, including depositing funds, paying bills, and writing checks.

- Highlight that taking over bill pay gives them one less thing to worry about

- Emphasize that they still own and have access to the funds

- Explain that because they retain ownership, the account funds don’t automatically pass to you upon their death. This enforces their independence and helps avoid misunderstandings with other family members later on.

- This account type offers mutual creditor protection: your creditors cannot gain access to the convenience account funds; and their creditors cannot access your funds.

Not all financial institutions offer convenience accounts, and even those who do only offer them in specific states. Other institutions have a concept of an “authorized signer”, which has similar benefits to a convenience account but often requires the person being added to have Power of Attorney (discussed next).

Remember to contact your specific branch for information before starting the discussion.

Power of Attorney

A Power of Attorney (POA) is a document that gives people, called agents, the power to act on behalf of another person, called the principal. There are nuances around the definitions and requirements for a POA between states, so be sure to consult the proper counsel in your state.

The general goal of a POA is to detail

- Who the principal is granting power to

- What exact powers those people have

- When the agent has the authority to use these powers

Setting up any type of POA is a significant decision that requires careful consideration and often legal guidance. Make sure to understand your fiduciary duties and their implications before agreeing to become your parents’ agent. Keep POA documents safe and make sure that the agents have access to the original documents.

Financial Power of Attorney

A POA can apply generally or be limited to a particular function. Limiting the scope of the agent to finances is called a Financial Power of Attorney. The document can include restrictions on which accounts your powers apply or can be written to allow you to represent your parents on all financial matters.

As a Financial POA, you’ll be able to perform financial tasks, like paying bills and filing taxes, on your parents’ behalf. Present the document to your parents’ institutions to establish access.

Durable vs. Springing Power of Attorney

The terms “Durable” and “Springing” both relate to when the agent has authority under the POA. Note that these terms and definitions may vary from state to state.

A Durable POA typically takes effect immediately and continues to be active if the principal becomes incapacitated. A non-durable POA would also start immediately but would only apply while the principal has the capacity to manage their finances. To be able to continue functioning as your parents’ POA late into life, you’ll likely need a Durable POA.

A Springing POA, sometimes called a conditional POA, allows the principal to define when the POA should take effect. The POA trigger is often the incapacitation of the principal, but could be any event or time. When defining a Springing POA, carefully define how to determine when the conditions for the POA are met. Any ambiguity could result in delayed acceptance of the POA validity.

- A common misconception is that the principal loses the ability to make decisions when they establish a POA. Remind them that they’ll still be able to access their funds and that the POA is a long-term safety net that enables short-term support.

- Discuss the different POA variations, noting how power can be limited.

- Suggest consulting with an elder law or estate attorney to ensure the POA meets their specific needs.

- Without a POA, your parents will receive a court-appointed conservator if they become incapacitated. Since your parents do not appoint the conservator, the court’s ruling may put strain on your family and make it challenging to ensure their wishes are met.

- Your parents may want to divide the POA responsibilities up amongst several people. This could mean appointing different people to be Medical POA and Financial POA or naming co-agents. If so, think through how the people receiving POA should make decisions, if the agents can act independently, and what each agent is responsible for.

- Emphasize that they may change or revoke the POA as long as they are competent.

Limitations

Being your parent’s POA does not automatically give you the power to manage your parents’ government benefits. The Social Security Administration (SSA) and Department of Veterans Affairs (VA) both have dedicated programs for managing another person’s benefits that require agency approval (discussed next).

SSA Representative Payee

If your parent receives Social Security benefits and are unable to properly manage these funds, becoming their Representative Payee (Rep Payee) may be appropriate. In this role, you petition the Social Security Administration (SSA) for the right to receive and manage SSA payments on their behalf. The SSA funds are managed in a dedicated account that lists your parents as the beneficiaries and you as their fiduciary. Importantly, although your parents own the funds in that account, they do not have the ability to access the account: only the Rep Payee has that ability.

As part of the Rep Payee responsibility, you need to file an annual report with the SSA about how the SSA payments have been spent. The SSA has strict and well-documented guidelines about how funds can be used and reported. Additionally, you need to report changes to your parents’ circumstance that may impact their eligibility for SSA benefits.

- This relationship removes your parents’ ability to directly access some of their funds. It’s important to be transparent and honest about this step with them and with the rest of the family. During this discussion, remind everyone that the funds will be managed in a dedicated account separate from your personal accounts

- Having access to the SSA funds allows you to pay bills, cover medical expenses, and provide funding for needs. Taking on these tasks gives your parents peace of mind they’re being handled correctly.

- The Rep Payee can give the beneficiaries spending money after core expenses have been met. Discussing this scenario might help overcome challenges about the lack of account access.

- SSA payments and interest generated by those payments are still owned by the beneficiaries (ie. your parents).

- If the beneficiary is deemed unable to manage their SSA benefits, the SSA will search for a Rep Payee. By initiating the process themselves, your parents have a good chance of receiving their desired representation. Note that the SSA must still approve the individual they choose.

- The SSA allows people to choose someone to serve as their Rep Payee in the future, if needed, through an “Advance Designation”. Setting this up yourself is a good way to bring up assuming the role on their behalf.

VA Fiduciary

A VA fiduciary is very similar to the SSA Rep Payee. This role is assumed when the beneficiary, one of your parents, is unable to properly manage Department of Veterans Affairs (VA) benefit payments. Once approved by the VA, you open a new account to manage the VA payments, naming your parents as the account beneficiaries and you as their fiduciary. All payments using this account must be made by check or electronic bill pay: you’re not permitted to withdraw funds from an ATM or make checks payable to cash.

The VA may inform you that you need to file annual fund usage reports or need to obtain a Corporate Surety Bond. Both of these requirements are meant to protect the beneficiary’s funds.

As a fiduciary, you have additional responsibilities. These include

- Ensuring all of the beneficiary’s bills are sent to you and paid on time

- Paying the beneficiary’s income taxes

- Collecting rent or unpaid debts

- Protecting the funds from creditors and loss

- Protecting the beneficiary’s private information

- Reporting changes in your, or the beneficiary’s, circumstance Refer to the VA for the full list of fiduciary requirements.

- This account relationship removes your parents’ ability to access the funds directly. It’s important to be transparent and honest about this step with them and the rest of the family. During this discussion, remind everyone that the funds will be managed in their own account, completely separated from your personal accounts

- Having access to the VA funds allows you to pay bills, cover medical expenses, and provide funding for needs. Taking on these tasks gives your parents peace of mind they’re being handled correctly.

- After paying the bills, the fiduciary can use any remaining funds to improve the beneficiary’s standard of living. This means your role won’t get in the way their fun, like taking a vacation or buying new furniture.

- If the beneficiary is deemed unable to manage their VA benefits, the VA will search for a fiduciary. By initiating the process themselves, your parents have a good chance of receiving their desired representation. Note that the VA must still approve the individual they choose.

Joint Account

A Joint Account is a shared bank account between you and your parents. All account holders have equal ownership and unrestricted access to the funds. This arrangement allows each party to deposit, withdraw, and manage the money without restriction. No account holder has a fiduciary duty to the others, meaning each person can use the funds as they see fit.

While Joint Accounts may sound convenient, they come with potential risks:

- Your parents’ money could be at risk if you face legal or financial troubles.

- Joint accounts typically have survivorship rights in most states that transfer ownership to the remaining account holder after the other passes. This may complicate distributing the account’s money to other beneficiaries.

- Relatedly, joint accounts can create tension with other family members who may perceive it as favoritism.

- All account holders can see all transactions, which may lead to privacy concerns and disagreements on spending.

You can mitigate, but not eliminate, some of the risks posed by Joint Accounts. Creating new accounts for the specific tasks you’re trying to help with, like paying bills or buying groceries, rather than adding your name to an existing account. When opening an account, write down its purpose and agreed-upon uses and have both parties sign the document. Aim to keep these account balances near zero and only add funds when needed. If the new account is held at the same institution as your parents’ funding account, transfers typically happen within a day. As always, be sure to regularly discuss account activity to maintain transparency and trust.

- Discuss the convenience of a Joint Account for managing regular expenses and bills.

- Be open about the potential risks and your commitment to using the account responsibly.

- Suggest starting with a small, separate Joint Account for specific purposes before considering larger accounts.

- Emphasize that this arrangement can be adjusted or ended if either party becomes uncomfortable.

- Consider the impact shared ownership of funds may have on the rest of the family.

If your parents are unable to manage their finances responsibly, to the extent that you believe restricting their access to money is necessary for their well-being, you may need to petition a court to become their conservator.

Conservator

The most responsibility you can assume for your parents is to become their Conservator, known as a Guardian in some states. This role is court-appointed and requires proving your parents, called Conservatees, are unable to manage their affairs and demonstrating why you are the right person to become the Conservator. Once appointed, conservators typically have training, reporting, and visitation requirements that vary by state.

It’s very important to understand how conservatorship differs significantly from other forms of financial caregiving:

- The conservatee does not choose the conservator or need to consent to the arrangement.

- A conservator may act against the conservatee’s wishes if it’s in their best interest.

- Some decisions require court approval before the conservator can act.

Conservatorship is typically considered only when less restrictive options are not viable because of the reduction in conservatee agency. The scope of a conservator’s power is outlined in the petition to the court. Conservator powers can be requested broadly or limited to specific areas. For example, a Conservator of Estate manages the conservatee’s financial affairs, while a Conservator of Person is responsible for the conservatee’s well-being and health. The court may appoint different individuals for each role based on their capabilities and the conservatee’s needs.

- Discuss conservatorship as a last resort, after other options have been explored. In particular, make sure you have exhausted discussions around appointing a Power of Attorney .

- Explain that this process involves the courts and may feel invasive, but it’s designed to protect vulnerable individuals.

- Be prepared for potential resistance or emotional responses, as the loss of autonomy can be distressing.

- Emphasize that the goal is to ensure their well-being and protect their interests when they’re unable to do so themselves.

- If possible, discuss conservatorship with other family members. Be sure to talk about the conservatorship’s impact on the family dynamic. Keeping everyone on the same page helps with your peace of mind and may prevent disagreements later on.

Remember, while conservatorship provides robust protection of vulnerable individuals from themselves, it also significantly restricts their autonomy. Conservatorship terminology varies by jurisdiction, and the process of becoming a conservator can be complex. Always consult with legal professionals and carefully consider all options before pursuing this path.

Conclusion

Taking on financial caregiving responsibilities for your parents can be daunting, but it’s also an opportunity to ensure their financial well-being and peace of mind. Understanding the continuum of account insight, access, and ownership options is an important part of supporting your parents’ needs over time. Before making any decisions, consider consulting a local elder-law or estate-planning attorney.

This transition can be emotionally challenging for both you and your parents. The shift in roles and responsibilities may bring up complex feelings. Approach the process with empathy and understanding, and don’t hesitate to seek emotional support if needed.

Remember: start gradually and increase involvement as needed. Always prioritize open communication and respect for your parents’ autonomy. Start the conversation early, be patient, and be prepared to adjust your approach as your family finds a process that works for everyone.

With thoughtful planning and open communication, you can successfully navigate this important transition together. Use the information in this article as a starting point for further research and in-depth family discussions. Every family’s situation is unique, and taking the time to explore and understand your options will help you find the best path forward for your parents’ financial care.